Main Report 2026

Germany is debating industrial policy. The debate is heated, urgent and involves billions. What this debate needs is a clear direction: the aim must be to strengthen innovation and entrepreneurial spirit in order to secure prosperity. This is also important because a strong economy is the foundation for democracy and the rule of law, for peace, freedom and social justice. However, such an economy can only exist through competition. This report examines what a competition-oriented economic policy might look like.

Many state interventions are costly and often ineffective. What is needed instead is vigorous competition and framework conditions that enable innovation.

Summary

-

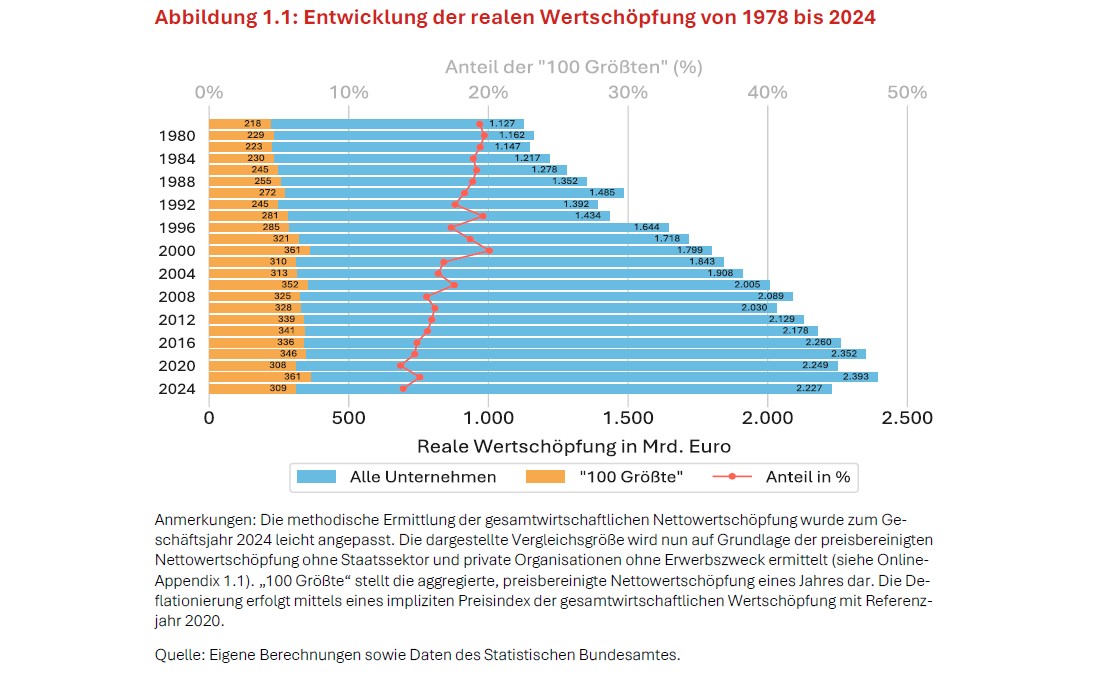

How is value added by the 100 largest companies in Germany developing, and how are they responding to changing business conditions?

Problem

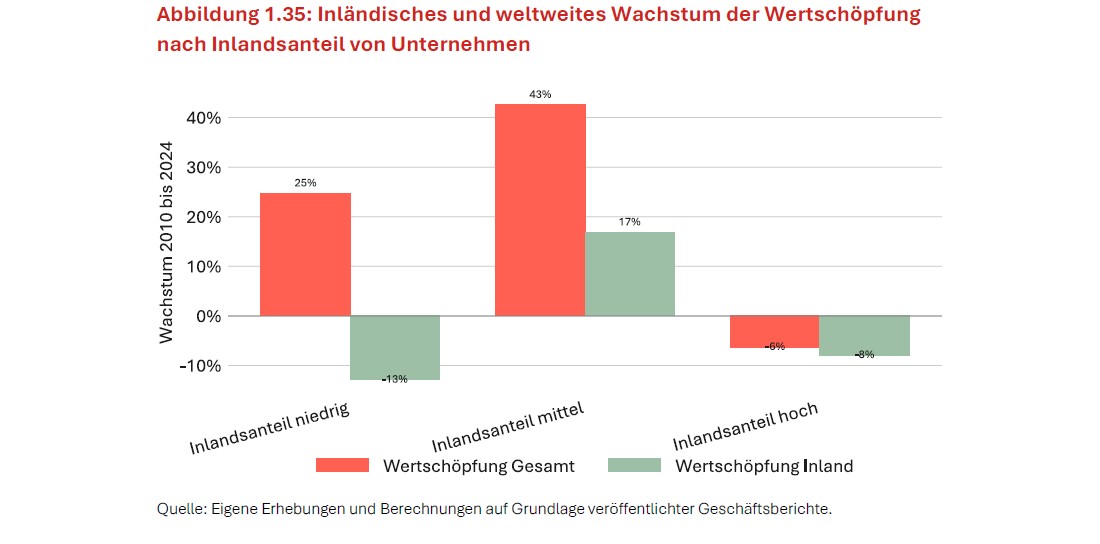

The report on market concentration shows that the 100 largest companies continue to be of great significance in terms of economic performance, employment and political influence, even though their aggregate shares of value added and employment have tended to decline over the long term. From a competition policy perspective, it is not so much size in itself that is problematic, but rather the possibility that economic power, political influence, ownership structures or personnel links may indirectly impair competition. At the same time, a large proportion of these companies are showing a decline in their domestic value-added. In the manufacturing sector in particular, global value added is growing faster than domestic value added, with the result that global corporate growth is becoming increasingly decoupled from Germany as a business location.

Context

The “Top 100” are identified on the basis of their domestic value added, in order to measure their macroeconomic significance in a way that is comparable across sectors. In 2024, their share of total economic value added stood at 13.9 per cent. At the same time, personnel links and merger activity remained evident, but were significantly lower than in previous decades when viewed over the long term.

An analysis of the “Top 100” excluding banks, insurance companies and foreign parent companies shows that the decline in the domestic share is occurring primarily in the manufacturing sector. These companies have often expanded globally, whilst domestic value added has stagnated or declined; this trend therefore points more to location- and structural issues than to a general weakness on the part of the companies.Recommendations

In the Monopolies Commission’s view, the relative shift of value added in the manufacturing sector abroad is a response to local conditions and is therefore driven not only by cyclical factors but also by structural ones. Growth abroad, particularly within the European single market, is, however, primarily an expression of free entrepreneurial decision-making and does not in itself constitute a competition problem. In the Monopolies Commission’s view, the shift only becomes relevant where avoidable, home-grown locational disadvantages distort such decisions. This gives rise to three recommendations:

- A competition-oriented industrial policy should examine the extent to which the weakness of the manufacturing sector stems from avoidable regulatory burdens and should remove such distortions without hindering market-driven adjustment processes.

- Where the state intervenes, it should prioritise the general framework conditions and take a horizontal approach, rather than protecting individual sectors or locations. This includes reducing regulatory components of energy prices, bureaucratic burdens and barriers to investment and adjustment.

- Sector- or company-specific support should only be provided where it addresses a clearly identified market or transformation failure and is designed in a way that is open to competition.

-

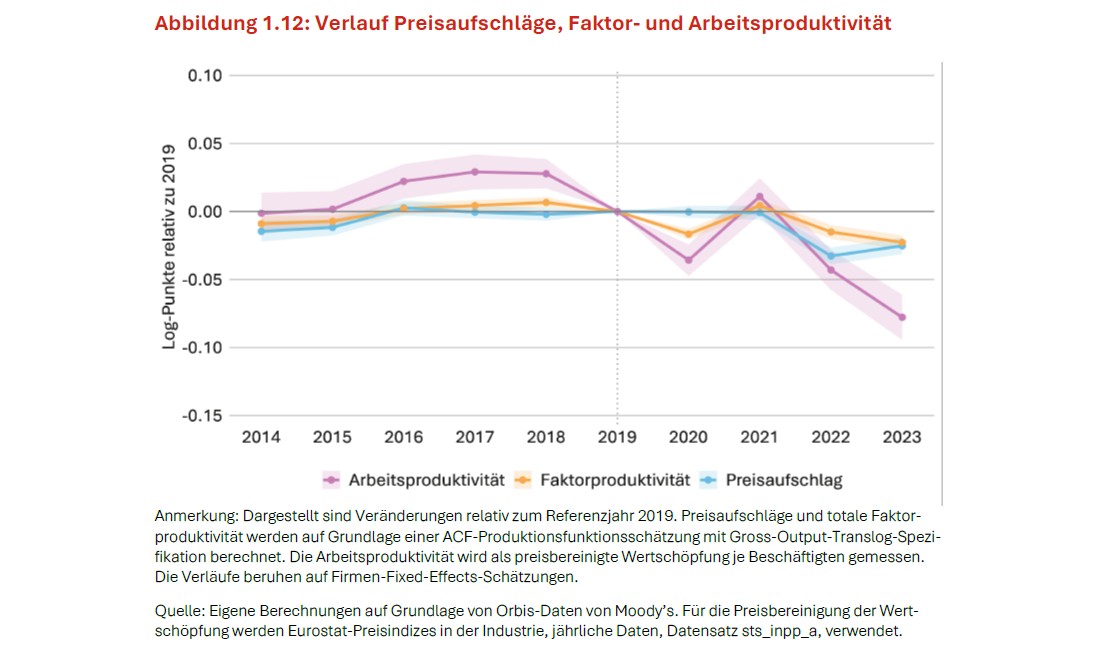

How has the energy price shock affected price mark-ups and productivity in the manufacturing sector?

How has the energy price shock affected price mark-ups and productivity in the manufacturing sector?

Problem

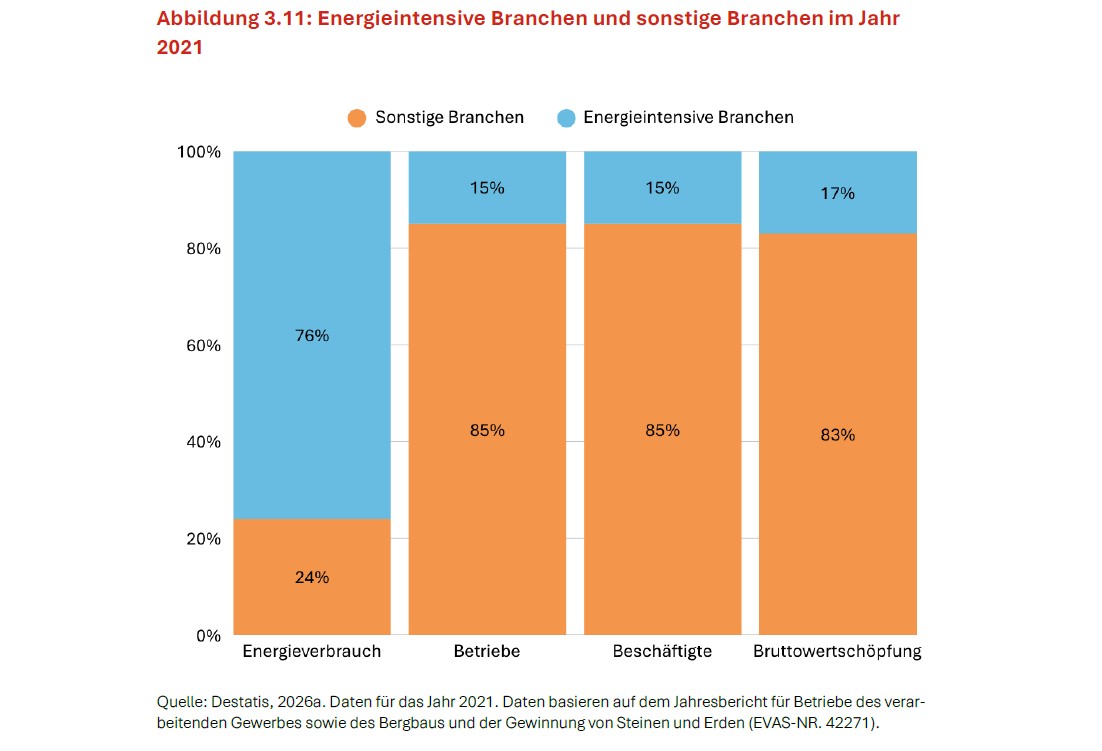

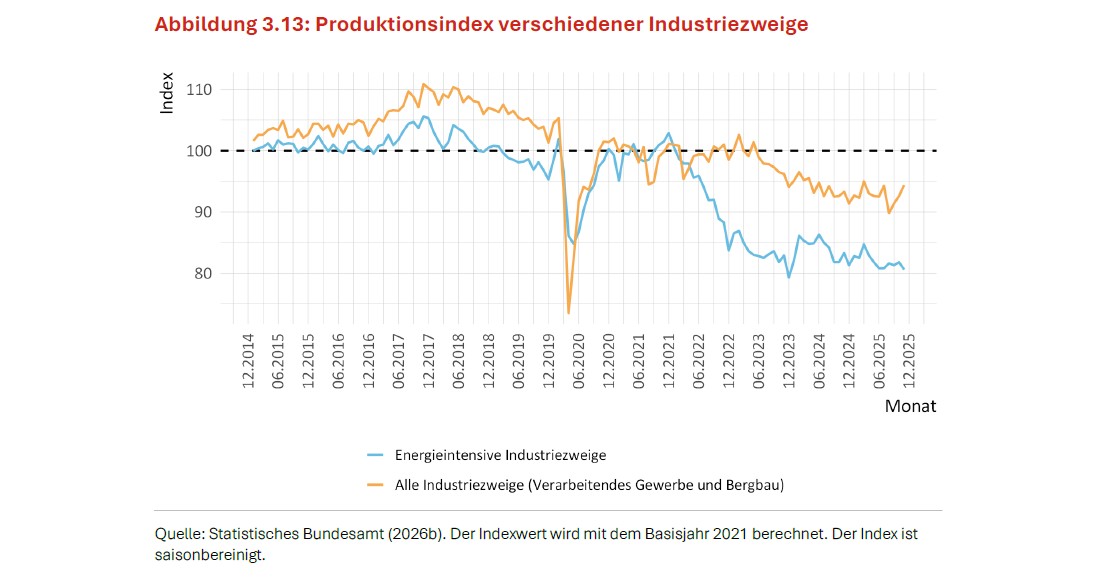

The energy price shock is more than just a temporary cost burden, particularly for the manufacturing sector. It is hitting an industry that has already been showing signs of a slowdown for several years. If certain sectors are less able than others to absorb rising costs or pass them on in the face of international competition, margins and productivity will fall and the prospects for the location will deteriorate. This could permanently alter Germany’s industrial structure and jeopardise prosperity.

Context

Signs of an industrial slowdown were already apparent before the recent crises. Since 2017, price-adjusted value added and labour productivity in particular have shown weaker growth. The crises of recent years have exacerbated this trend. Since 2021, price mark-ups in the manufacturing sector have also fallen significantly. Although prices rose significantly overall by 2023 compared with 2019, companies’ costs increased even more sharply and could only be passed on to a limited extent.

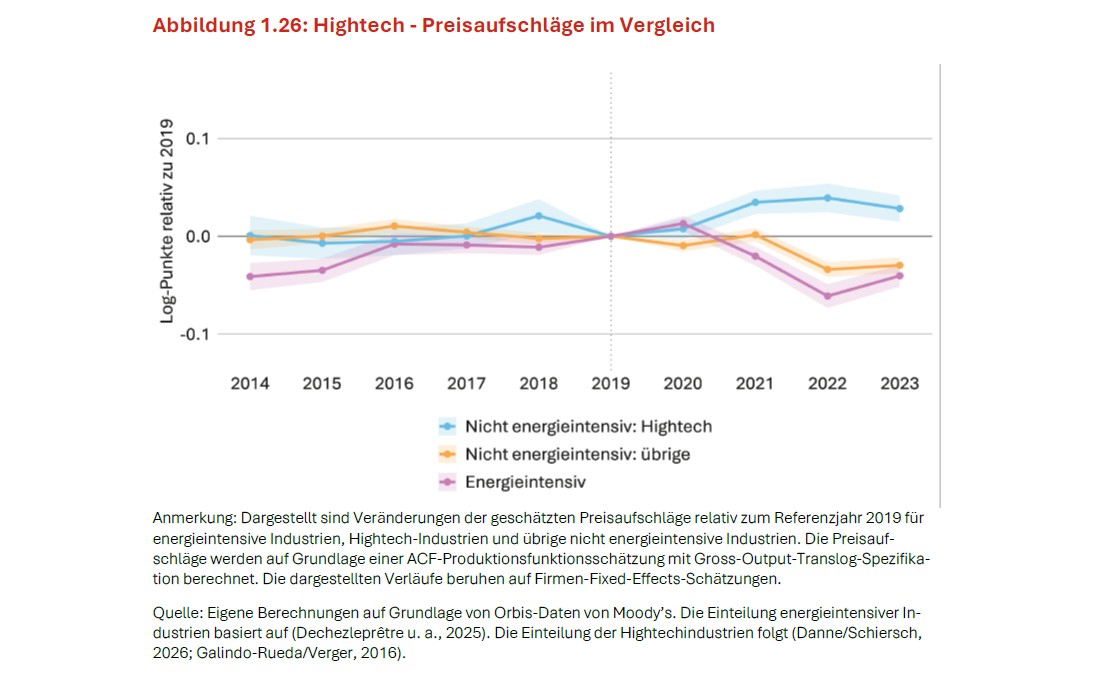

At the same time, a clear divide is evident within the manufacturing sector. In energy-intensive industries, costs rose more sharply and productivity and price mark-ups fell more significantly than in non-energy-intensive industries, which proved to be more resilient overall. High-tech sectors, by contrast, recorded rising price mark-ups and productivity, but were unable to keep pace in an international comparison.

International integration also plays a role. Higher import intensity was associated with more favourable trends in non-energy-intensive industries. In energy-intensive industries, the results also point to possible substitution effects vis-à-vis domestic intermediate goods production. Higher export intensity tended to be accompanied by weaker trends in price mark-ups. Comparatively similar trends in employment, despite differing developments in value added, also point to labour market rigidities.

Recommendations

Competitive location conditions determine whether industrial capacity in the manufacturing sector can be productively renewed or whether it comes under sustained cost pressure. At the same time, location conditions influence how international trade linkages play out. Imports can cushion cost rises, but they can also displace domestic intermediate goods production if domestic production conditions remain uncompetitive in the long term. From the Monopolies Commission’s perspective, this gives rise to two recommendations:

Policy-makers should take a long-term view and improve general business conditions. Market-driven structural changes should not be held back by the permanent protection of existing structures.

Labour market policy should facilitate occupational mobility and effective competition for skilled workers. Barriers to mobility and recruitment should be removed. This also includes examining the extent to which employment protection rules and non-wage labour costs hinder mobility and recruitment. Digital and AI-related skills, along with an innovation-oriented mindset, should be fostered at an early stage.

-

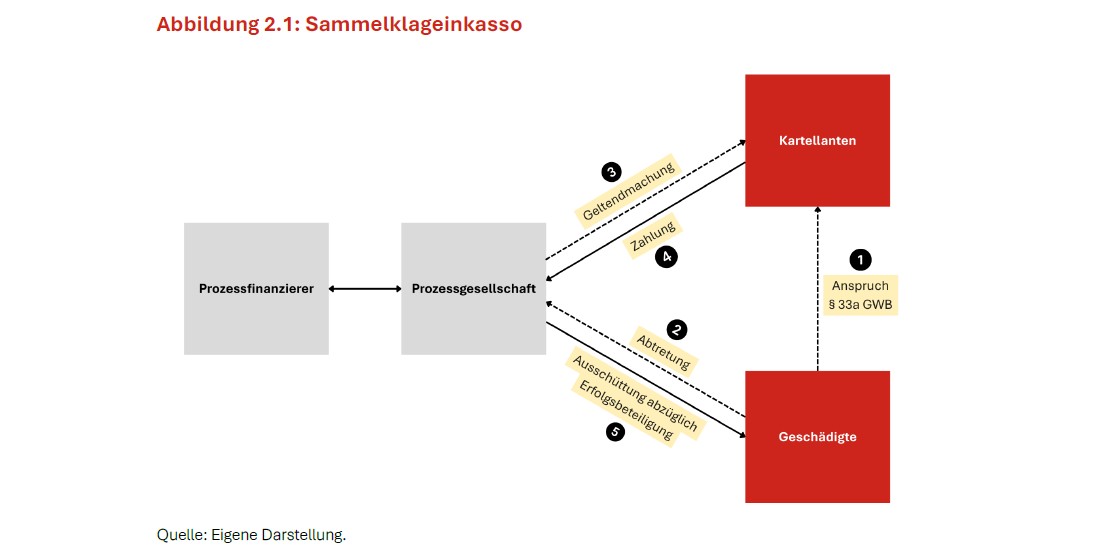

How can claims for damages under competition law be enforced more effectively in practice?

Problem

The practical enforcement of claims for damages arising from antitrust infringements remains difficult. It is often not economically viable to pursue claims for smaller, scattered losses, as the individual loss is minimal whilst the costs of litigation are high, and companies have so far lacked a legally secure instrument for collective enforcement. Furthermore, quantifying the amount of damages is particularly challenging because the hypothetical competitive price that would have prevailed in the absence of the antitrust infringement cannot be observed, and econometric expert reports often lead to costly and protracted disputes in practice.

Context

Antitrust damages compensate for losses whilst at the same time strengthening the enforcement of competition rules. However, despite the legal framework set out in sections 33a et seq. of the German Act against Restraints of Competition (GWB), its practical enforcement remains complex, fraught with legal uncertainty and protracted. At the same time, recent decisions by higher and supreme courts show that more practical approaches and legal certainty are gradually emerging on key legal issues such as the consolidation of claims and the assessment of damages.

Recommendations

Against this background, the enforcement of claims for damages arising from antitrust infringements should be further improved. The Monopolies Commission recommends:

- The courts should permit the use of existing instruments for the consolidated enforcement of claims for scattered damages in the interests of effective enforcement of the law. Class action recovery – which has been available with legal certainty since the Federal Court of Justice’s ruling – can help ensure that even smaller claims for damages arising from antitrust infringements can be pursued and that victims do not remain structurally at a disadvantage compared to the infringing parties.

- When estimating damages, the courts should, depending on the individual case, draw on econometric regressions or more flexible estimates based on a sound factual foundation. Regression analyses may be appropriate in suitable cases, but must not effectively become a prerequisite for claiming antitrust damages if the available data or the principles of procedural economy argue against it.

- The procedural framework should be further developed to make antitrust damages proceedings more efficient, faster and more manageable. In particular, this can be achieved by grouping similar cases more closely together, further concentrating jurisdiction and providing the courts with effective tools for dealing with voluminous case files.

-

How can procurement and market structures in the defence sector be kept open to competition?

Problem

Competition in the defence sector is structurally constrained. Outdated security and industrial policy considerations on the part of Member States hinder open competition. Joint ventures between established manufacturers and defence conglomerates can reinforce dependencies and further hinder market access for smaller suppliers. This is without prejudice to the fact that cooperation between companies may be objectively justified for the necessary rearmament and is not, in principle, precluded under competition law.

Context

In light of the changing security landscape and rising defence spending, the defence sector has become significantly more important – both in Germany and at European level. This is precisely why it is vital to ensure that the necessary rearmament is carried out efficiently. Competition is essential to this end.

Recommendations

Against this background, competition in the defence sector should be specifically strengthened and competitive risks should continue to be closely monitored:

- Cooperation and mergers in the defence sector should be carefully assessed under competition law. This applies in particular to joint ventures between established manufacturers and diversified defence conglomerates, which can raise barriers to market entry and increase dependencies.

- A more far-reaching sector-specific exemption for the defence sector under competition law should not be introduced. The current law does not, in principle, preclude necessary cooperation, whilst blanket relaxations could entrench inefficient structures and weaken incentives for innovation.

- Defence procurement should become more competition-oriented and innovation-friendly. Joint procurement, greater interoperability, greater involvement of start-ups and SMEs, and simpler and faster procedures can better harness competitive potential.

-

How should competition policy respond to rising fuel prices?

Problem

Following the outbreak of the Iran war and the blockade of the Strait of Hormuz, the supply of crude oil and petroleum products became scarce, which also led to a rise in fuel prices in Germany. However, the rise in prices in Germany – which was above the European average and, above all, more rapid – is likely to be attributable not only to the cost shock but also to structural competition problems in the intermediate markets (refineries and fuel wholesalers).

Context

The legislature has responded to the rises in fuel prices with a series of measures designed to address the competition issues in the wholesale markets, which are also the subject of the Federal Cartel Office’s ongoing proceedings under Section 32f of the Act against Restraints of Competition (GWB). In addition, measures such as the ‘12 o’clock rule’ and the ‘petrol discount’ were introduced, which directly intervened in price formation on the fuel markets.

Recommendations

Against this background, the Monopolies Commission recommends, above all, addressing the structural competition problems in the wholesale markets and at the refinery level:

- The Federal Cartel Office should vigorously pursue the proceedings it has initiated under Section 32f of the Act against Restraints of Competition (GWB), using the instruments and data at its disposal. In this regard, the new data collection in accordance with Section 47k(7) of the draft 12th Amendment to the Act against Restraints of Competition (GWB-E), as proposed in the draft bill, can improve the data basis. In principle, however, the necessary data should be collected in the respective proceedings.

- Sustainable structural solutions are preferable to sector-specific market interventions and price controls that are questionable from a regulatory perspective. It is doubtful whether the proceedings under the newly introduced Section 29a of the GWB are significantly faster and more effective than structural measures.

- Interventions in free price formation, such as the ‘petrol discount’, should be avoided in future because they are costly, provide asymmetric relief and, above all, dampen price signals caused by scarcity. The fuel discount was not passed on in full to consumers. Regional differences in the extent to which it was passed on point to competition issues. The ‘12 o’clock rule’ should be evaluated and, if necessary, further developed.

-

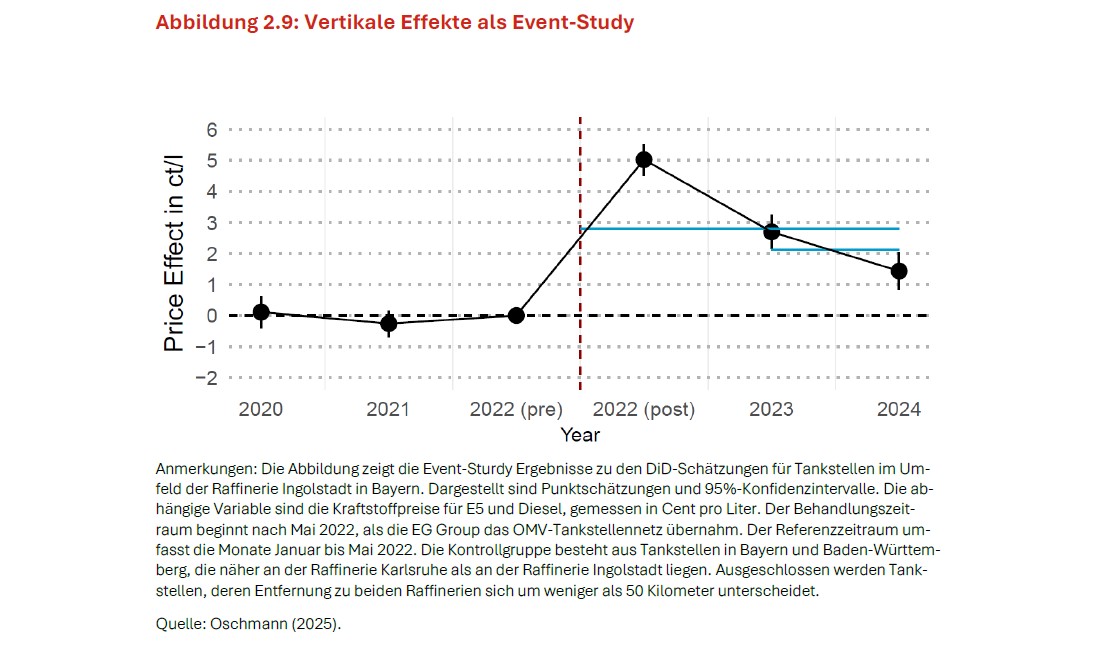

How can ex-post evaluations contribute to the evidence-based development of merger control and competition policy?

Problem

Merger control is always a decision made under conditions of uncertainty, because the competitive effects of a merger can only be assessed on a predictive basis prior to its implementation. Without ex-post evaluations, it therefore often remains unclear whether the assessment tools used were appropriate and whether the underlying mechanisms of impact, as well as any remedial measures, accurately reflected actual market developments.

Context

The study on the merger between OMV and EG Group, summarised here by way of example on the basis of the ex-post evaluation, shows that price effects in the petrol station market cannot be explained solely by local competition between petrol stations. Rather, the results suggest that the observed price increases are primarily linked to changes in vertical supply structures and refinery supply. Ex-post evaluations bring such mechanisms to light and can thus help to better target merger control, market monitoring and crisis management policies.

Recommendations

Against this background, ex-post evaluations should be utilised more extensively as a tool for an adaptive and evidence-based competition policy:

- Ex-post evaluations should be used systematically to draw lessons from past decisions for future proceedings and to further develop merger control on an evidence-based basis. They make it possible to test prognostic assumptions retrospectively against actual market developments, thereby promoting institutional learning.

- Ex-post evaluations should be based on a transparent and robust empirical methodology. In particular, a comprehensible counterfactual design is required, one that discloses comparison groups, time periods and control variables, thereby enabling robust conclusions to be drawn about the effects of a merger.

- The results of ex-post evaluations should be systematically incorporated into future merger control proceedings, assessment tools and remedial measures. The case study provided as an example demonstrates that ex-post evaluations can yield additional insights into the competition mechanisms that are actually effective.

-

How can industrial policy and competition policy work together to strengthen the competitiveness of the European single market?

Problem

The European single market and Germany as an industrial hub are under considerable pressure to adapt. Geopolitical tensions, dependencies in critical supply chains, rising energy costs and the need for decarbonisation are increasing the pressure to act. Added to this are structural weaknesses such as a growing innovation gap compared with the US and China, a shortage of skilled workers, as well as heavy regulatory burdens and protracted approval procedures.

Context

Industrial policy is intended to influence economic development in a targeted manner and is currently understood, above all, as a response to a lack of innovation, transformation and geopolitical vulnerability. A distinction must be made between horizontal measures, which improve the framework conditions for many businesses, and vertical interventions, which specifically support individual sectors, technologies or companies. From the Monopolies Commission’s perspective, this distinction is crucial: horizontal measures tend to strengthen the single market, whilst vertical interventions interfere more heavily with market processes and pose greater risks to competition, innovation and the allocation of resources. However, the latter are not to be ruled out – provided they address a clearly diagnosed market or transformation failure and remain open to competition, transparent and time-limited.

Recommendations

The Monopolies Commission regards competition as an indispensable part of a successful industrial policy. This gives rise to three policy priorities:

- Industrial policy measures should focus on clearly justified cases of market or transition failure and be primarily geared towards future-oriented and strategically important key technologies.

- Measures to complete the European single market should take precedence, as it is precisely there that better framework conditions for innovation, scaling up and competition can be created for all businesses.

- Where support is provided to individual sectors or technologies, the instruments should be open to competition, transparent, coordinated at European level and, where possible, time-limited.

-

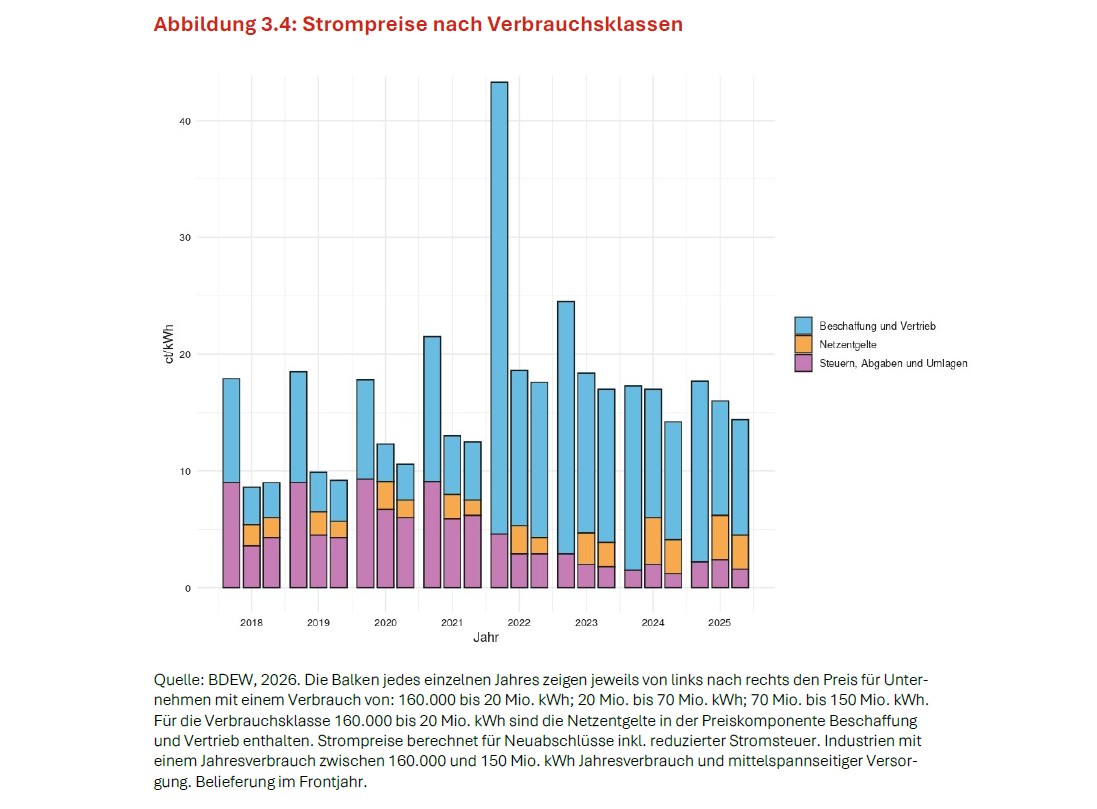

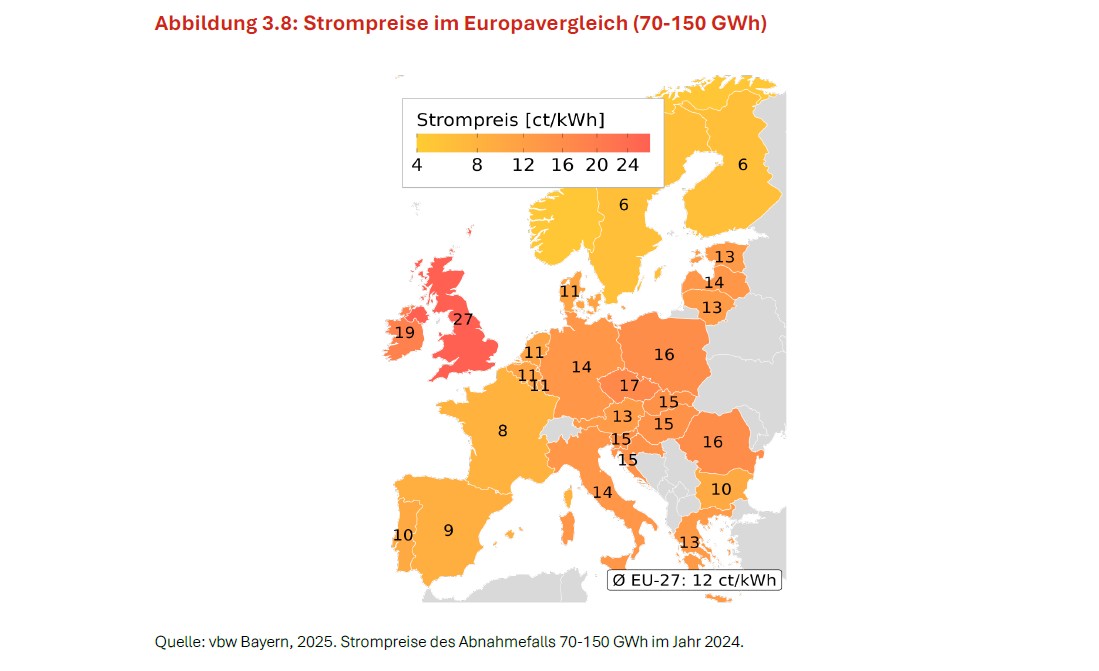

How can the competitive environment for German industry be improved with regard to the cost of electricity?

Problem

High electricity prices are putting a strain on German industry in the face of international competition. In 2024, Germany’s average price of around 14 ct/kWh was above the EU-27 average of 12 ct/kWh and significantly higher than that of the USA at 8 ct/kWh. This is particularly relevant for electricity-intensive sectors such as aluminium production. If electricity, as a key factor of production, is permanently more expensive than in key competitor regions, investment and value creation could increasingly be shifted abroad.

Context

Electricity is a significant cost factor for industry, but its importance varies greatly from sector to sector. On average across all 163 sectors examined, the direct share of electricity in intermediate consumption is only 2.29 per cent. In many sectors, it is below 5 per cent, whilst in certain industries, such as aluminium or pulp, it exceeds 15 per cent. At the same time, there is already a dense network of vertical relief measures such as electricity price compensation, the industrial electricity tariff, reductions in electricity tax and subsidies towards grid charges. These measures operate according to different criteria, create red tape, sometimes put smaller companies at a disadvantage and pose risks to competition. The simulation in this chapter also shows that the overall price effects of various subsidy scenarios differ only slightly.

Recommendations

With a view to improving the competitive conditions for German industry with regard to the cost of electricity, the Monopolies Commission has identified the following policy priorities:

- Where relief from electricity prices is sought, priority should be given to horizontal, straightforward measures that do not undermine competition. These include, above all, broad-based relief on non-market-determined components of electricity prices.

- Sector-specific or company-specific relief measures – such as electricity price compensation, an industrial electricity tariff or subsidies towards grid charges – should only be used in a targeted and strictly limited manner. They should be clearly justified on objective grounds, designed as simply as possible and structured in such a way that they do not distort competition.

- The electricity market design should be reformed so that electricity can be supplied in a structurally cheaper and more reliable manner. As high prices also result from systemic weaknesses such as grid bottlenecks, inadequate price signals and high redispatch and grid costs, state aid is no substitute for reforming the system. In particular, grid tariffs should be reformed, incentives for grid-friendly behaviour strengthened and the grids further digitised.

-

How can Germany accelerate the AI transformation of industry in a way that promotes competitiveness?

How can Germany accelerate the AI transformation of industry in a way that promotes competitiveness?

Problem

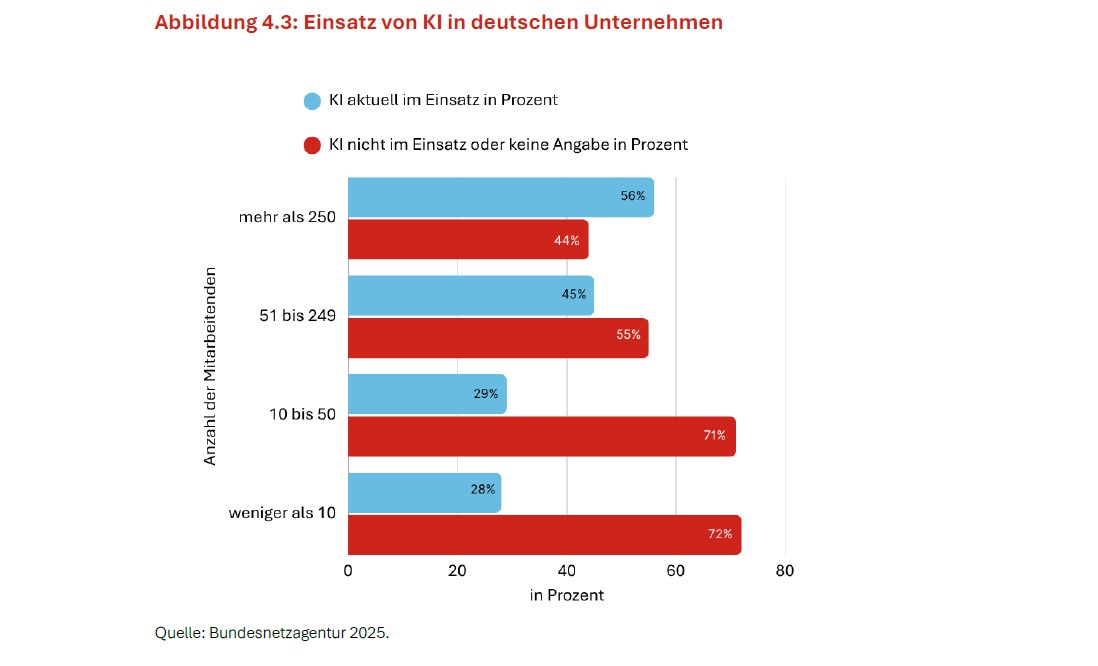

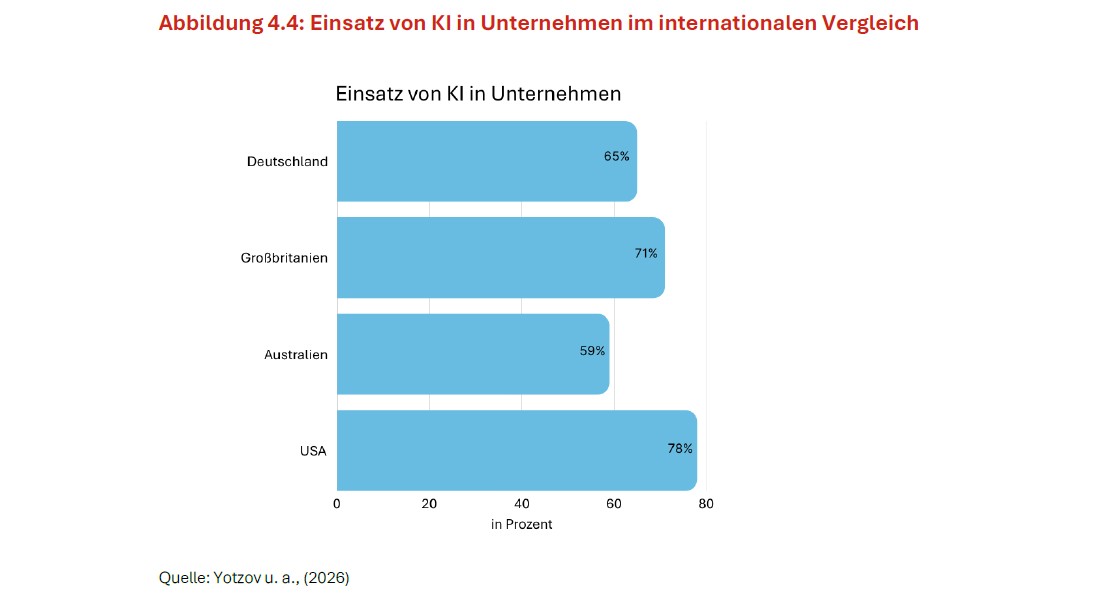

The AI transformation of German industry is not progressing on the necessary scale. Three factors in particular are holding back the AI transformation of German industrial companies: significant business and legal uncertainty, a reluctance to take risks with long-term investments, and sluggish organisational processes within the companies themselves. If these obstacles persist, there is cause for concern that German industry will fall further behind in terms of productivity, competitiveness and value creation.

Context

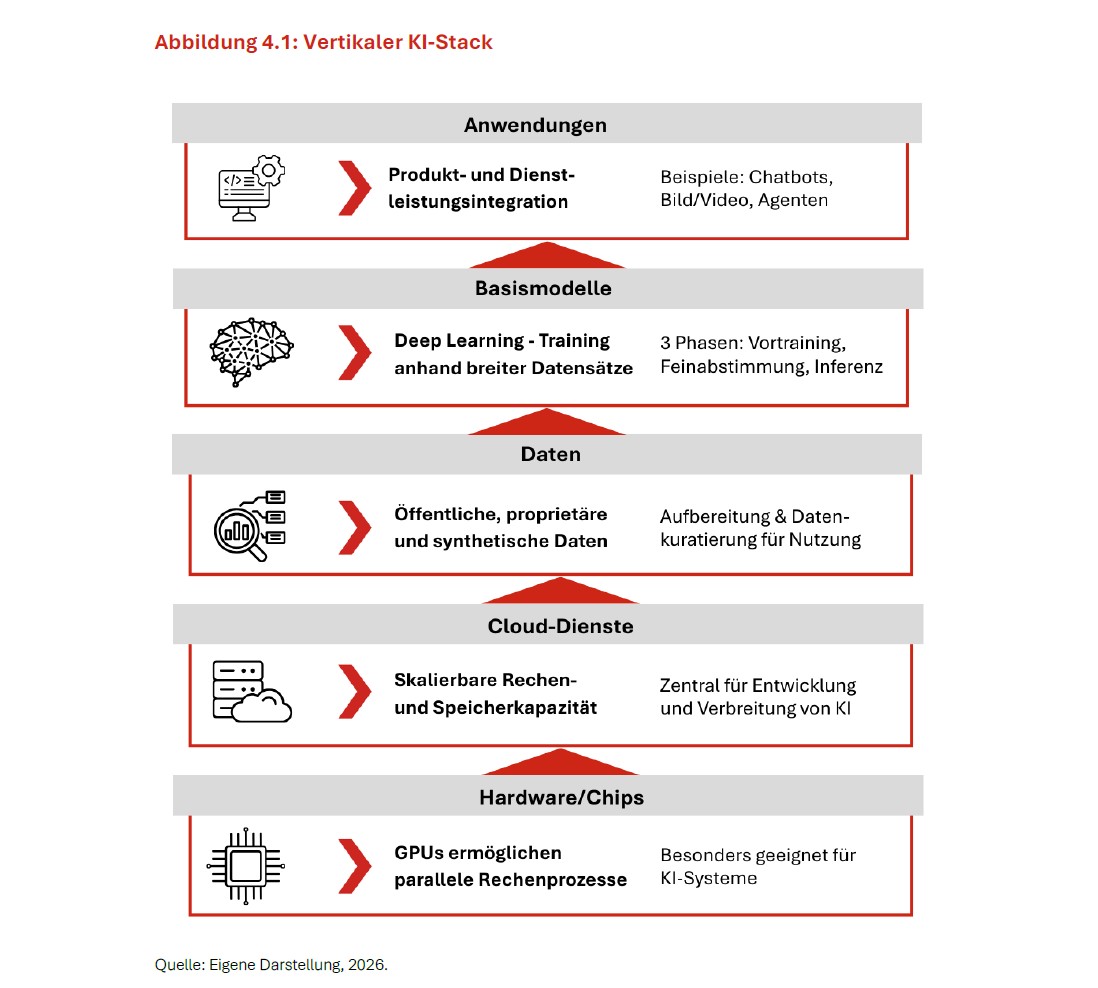

The AI transformation is taking place against a backdrop of sluggish growth, geopolitical tensions and existing locational disadvantages in Germany and Europe. AI is a cross-cutting technology with considerable potential for innovation, efficiency and new competitive advantages. However, this potential is not freely available: the core layers of the AI stack are dominated by a small number of providers, most of whom are based outside Europe. This creates dependencies. At the same time, adoption is progressing too slowly and on too narrow a scale. As market forces alone have so far failed to generate the necessary speed and breadth, there is considerable pressure for economic policy action. It is therefore crucial to take action at the right level. The real competitive advantage of German industry lies not in the stack itself, but at the application level: in specialist knowledge built up over decades and valuable data from its own production processes. Harnessing and protecting this advantage is the central task of economic policy.

Recommendations

The AI transformation requires a competition-oriented economic policy that makes targeted use of government intervention without undermining competition. To this end, three pillars should be consistently aligned: competition policy, regulation and industrial policy.

- Competition policy: The Digital Markets Act (DMA) should be adapted to address new competition risks across the AI stack and enforced resolutely. This involves, in particular, focusing on AI services and further developing behavioural obligations in such a way as to ensure open and contestable markets, whilst limiting tendencies towards market foreclosure through vertical integration, self-preferencing and exclusive access to key AI resources. In areas where the DMA does not apply, Section 19a of the German Act against Restraints of Competition (GWB) provides the Federal Cartel Office with the flexibility and scope to intervene.

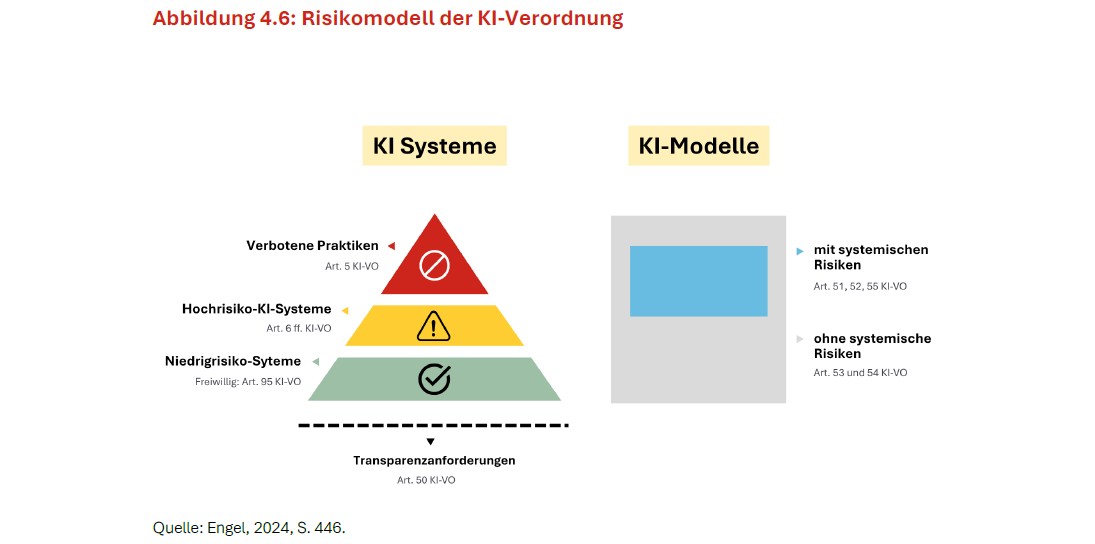

- Regulation: The EU AI Act is, in principle, the right approach and an important step as a uniform European legal framework. However, it should be implemented and further developed in such a way as to avoid unnecessary burdens on innovation and diffusion. In general, a paradigm shift in government regulation should be initiated – moving away from attempts at early and comprehensive regulation of new technologies towards regulation that only comes into effect once experience has been gained in the markets. Particularly for small and medium-sized enterprises, disproportionate compliance burdens, double regulation and uncertainties regarding risk classification should be mitigated, so that the AI Act creates legal certainty without hindering the widespread use of AI.

- Industrial policy: Industrial policy should not promote individual national or European ‘champions’, but rather enhance the widespread use of AI. Where high risks, dependencies or coordination problems exist, the state should act in a targeted manner as an anchor customer for European and German AI solutions, thereby supporting demand, testing and scaling. To ensure the widespread adoption of AI, IP transfer processes from research institutions should be accelerated and AI-related skills development strengthened.

Further downloads

- Summary PDF, 13 MB (not accessible)

- Kurzfassung PDF, 13 MB (not accessible)

- Kapitel 1: Konzentrationsberichterstattung PDF, 5 MB (not accessible)

- Kapitel 2: Kartellrechtliche Entscheidungspraxis PDF, 4 MB (not accessible)

- Kapitel 3: Industriepolitik und Strompreise PDF, 3 MB (not accessible)

- Kapitel 4: KI-Transformation PDF, 1 MB (not accessible)

- Online-Appendix PDF, 1 MB

- Hauptgutachten 2026 PDF, 15 MB

Graphs

Episode 19: 2026 Main Report: Towards a competition-oriented economic policy

Episode 19: 2026 Main Report: Towards a competition-oriented economic policy

Tomaso Duso and Elif Senel discuss the findings of the 2026 main report on our Cast4Competition podcast.